Most travel insurance claim guides tell you to save receipts, confirmations, and records.

That advice is useful — but it is not enough.

A receipt may prove you paid for something. A cancellation email may prove a trip component changed. A delay screenshot may show that a flight was late.

But none of those automatically prove that the claim is covered.

That is where travelers can get caught off guard. Travel insurance claims are not only about what happened. They are about whether your documents prove the right things: the event, the reason, the cost, and the amount you could not recover somewhere else.

The real question is not just:

“What documents do I need?”

It is:

“What does each document need to prove?”

This guide explains what travel insurance claim proof usually needs to show, why receipts alone may not be enough, and what to save before you file a claim.

Quick Answer

What proof do you need for a travel insurance claim?

Travel insurance claim proof usually needs to show what happened, why it happened, what it cost, and what amount was not refunded, credited, reimbursed, or recoverable elsewhere. The exact documents depend on the claim type, but receipts alone may not be enough.

A strong claim file may include booking confirmations, proof of payment, receipts, cancellation notices, medical records, airline delay statements, baggage reports, refund records, provider emails, claim forms, and written proof connecting the loss to the reason for the claim.

System Insight

Travel insurance claims usually require more than proof of payment.

A receipt may show that you spent money, but it does not always prove the expense was covered, necessary, non-refundable, or caused by a qualifying event. The strongest claim files connect the disruption, the policy reason, the cost, and the unrecovered loss.

- Receipts can prove what you paid.

- Provider statements can help prove what happened and why.

- Refund records can show what you did or did not recover.

- Policy language determines whether the proof supports a covered claim.

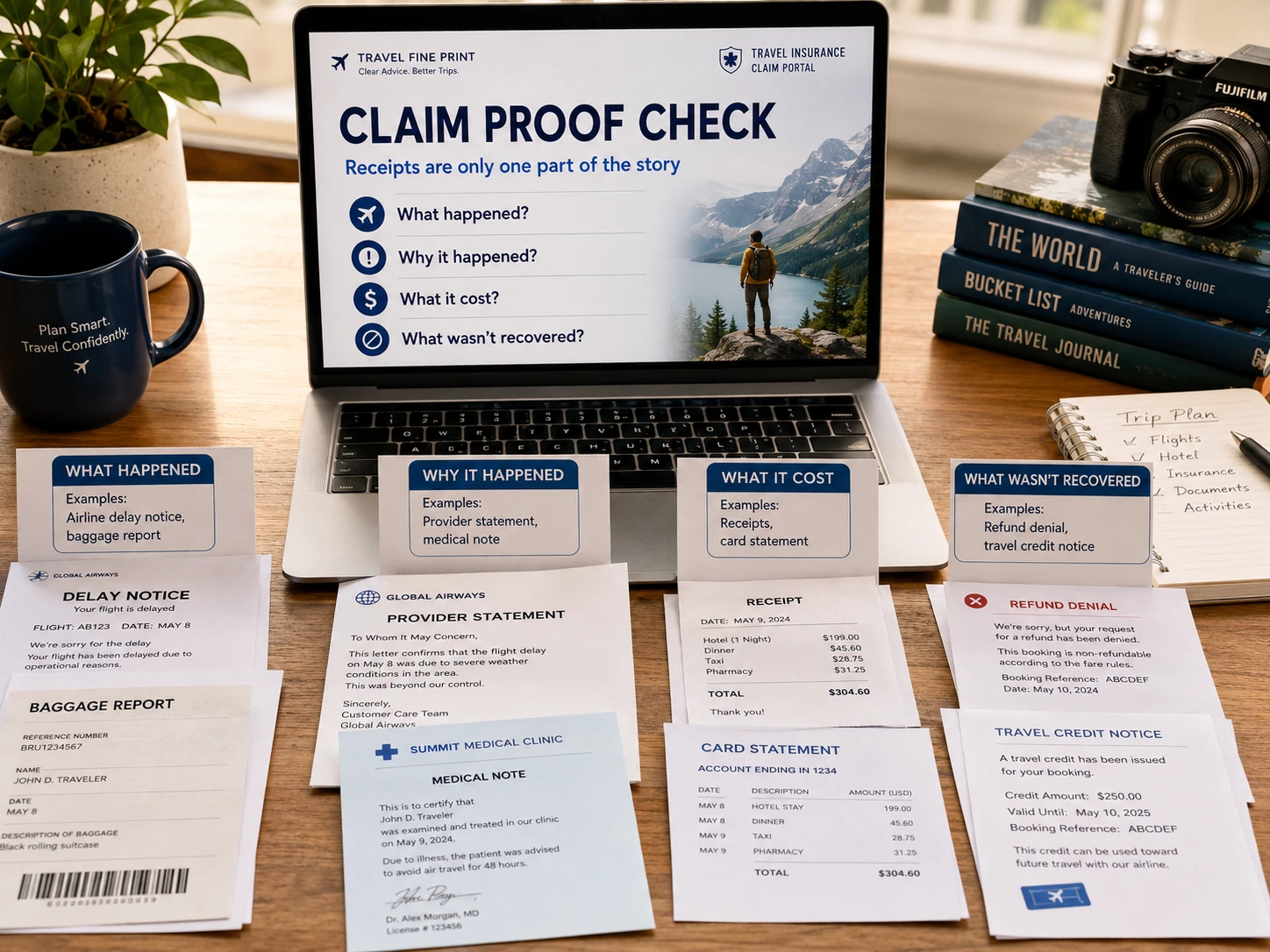

The Four-Part Claim Proof Test

A travel insurance claim file is strongest when the documents answer four separate questions.

Most travelers focus on the third one — what did it cost? — because receipts are the easiest proof to understand. But the insurer may also need to see what happened, why it happened, and what amount was actually unrecovered after refunds, credits, or provider reimbursements.

That is why a pile of receipts can still leave a claim weak if the paperwork does not connect the full story.

What happened?

The event, delay, cancellation, illness, baggage issue, accident, or disruption that triggered the claim.

Why did it happen?

The reason that may connect the event to a covered situation in the policy.

What did it cost?

The amount paid, charged, lost, or spent because of the travel problem.

What was not recovered?

The amount not refunded, credited, reimbursed, waived, or recoverable from another source.

Proof of What Happened

The first job of your claim file is to prove that the travel problem actually happened.

This might sound obvious, but many travelers rely on their own explanation instead of saving third-party proof. A statement like “my flight was delayed” or “my bag did not arrive” may not be enough by itself. The insurer may want documentation from the airline, hotel, cruise line, tour operator, medical provider, police department, or another source connected to the event.

For a flight delay, that might mean a written airline delay statement, cancellation notice, updated itinerary, or boarding pass. For baggage problems, it might mean a property irregularity report, baggage claim number, delivery record, or written confirmation from the airline. For a medical issue, it may mean treatment records, itemized bills, or a physician statement.

The goal is to show that the disruption was real, documented, and tied to your trip.

A good rule: the closer the document is to the source of the problem, the stronger it usually is.

Proof of Why It Happened

This is where many travel insurance claims become harder.

It is not always enough to prove that something happened. The insurer may also need to know why it happened, because the reason must connect to a covered event in the policy.

For example, a flight delay may be treated differently depending on whether it was caused by weather, mechanical issues, crew availability, air traffic control, or another reason. A trip cancellation may be treated differently depending on whether it was caused by illness, injury, a work conflict, fear of travel, a changed plan, or a provider cancellation.

That is why official wording matters. A screenshot showing that a flight was late may help, but it may not prove the official reason for the delay. A cancellation email may show that a booking was canceled, but it may not prove the covered reason behind the cancellation.

For medical claims, the reason may need to be documented by a doctor, clinic, hospital, or other medical provider. For theft or accident claims, the insurer may ask for a police report, incident report, or other official record.

The fine print issue is simple: the reason for the loss often matters as much as the loss itself.

Proof of What It Cost

Once the event and reason are documented, the claim also needs to show the amount you paid, lost, or spent.

This is where receipts, invoices, booking confirmations, credit card statements, and itemized bills matter. But even here, the details count.

A receipt, invoice, booking confirmation, or card statement is strongest when it clearly shows the date, merchant, amount, and travel component connected to the claim. If the document only shows a vague charge, the insurer may ask for more detail.

For extra expenses caused by a covered delay or interruption, itemized receipts are usually stronger than general card charges. A meal receipt, hotel invoice, taxi receipt, prescription receipt, or replacement-item receipt should show the date, amount, merchant, and what was purchased.

The stronger the money trail, the easier it is to connect the claim amount to the disruption.

Proof of What You Could Not Recover

This is one of the most overlooked parts of travel insurance claim proof.

Travel insurance usually does not want to pay for a loss that was already refunded, credited, waived, reimbursed, or recoverable from another source. That means your claim file may need to show not only what you paid, but also what you did not get back.

This can include cancellation confirmations, refund denial emails, partial refund records, travel credit notices, airline or hotel refund statements, cancellation-policy screenshots, or provider emails explaining that a charge was non-refundable.

This matters because a traveler may think, “I lost $1,200,” while the insurer may ask, “How much of that was actually unrecovered after refunds, credits, or provider reimbursement?”

A travel credit can also complicate the claim. Even if you wanted cash back, the insurer may treat a credit differently than a total loss depending on the policy and situation.

The hidden claim question is not just:

“What did you pay?”

It is:

“What amount is still actually lost?”

Weak Proof vs. Stronger Proof

Not all documentation carries the same weight.

A screenshot, receipt, or short email may help, but it may not prove the full claim by itself. Stronger proof usually comes from a source connected to the event, shows the date and details clearly, and explains the reason, amount, or refund status in writing.

The goal is not to overwhelm the insurer with every document you have. It is to submit proof that connects the claim clearly enough that the reviewer can follow what happened, why it happened, what it cost, and what remains unrecovered.

Weaker Proof

May help, but may not prove enough

- A receipt that shows a charge but not why the expense was necessary.

- A screenshot showing a delay but not the official reason or duration.

- A cancellation email that does not explain why the trip was canceled.

- A booking confirmation that does not show payment, refund status, or cancellation terms.

- A general explanation from the traveler without third-party support.

Stronger Proof

Helps connect the event, reason, cost, and loss

- An airline or provider statement showing what happened and why.

- Itemized receipts showing date, merchant, amount, and what was purchased.

- Medical records or physician documentation tied to the travel disruption.

- Refund, credit, or denial records showing what was not recovered.

- Policy language, claim forms, and supporting documents organized by date.

The strongest claim file is not always the largest file.

It is the clearest one.

If the reviewer can see the event, the reason, the cost, and the unrecovered loss without guessing, the claim is usually easier to evaluate. If the documents leave gaps, the claim may be delayed while the insurer asks for more information — or denied if the missing proof is essential.

Traveler Risk

A receipt alone may not prove a travel insurance claim.

A receipt can show that you paid for something, but it may not show why the expense happened, whether the reason was covered, whether the cost was necessary, or whether the amount was non-refundable. If the paperwork does not connect those pieces, the claim may be delayed, reduced, or denied.

Build the Claim File While the Problem Is Happening

The hardest proof to get is usually the proof you did not ask for at the time.

After the trip, it may be difficult to get an airline to explain the official reason for a delay, a hotel to confirm a non-refundable charge, a tour operator to document a cancellation, or a provider to put refund status in writing.

That is why the best time to build a travel insurance claim file is while the disruption is still happening.

Before you leave the airport, hotel, clinic, baggage office, or provider desk, ask for written confirmation of what happened, why it happened, and what costs or refunds are involved.

Action Step

Save proof before you file the claim.

Do not wait until the claim form asks for documents. Start saving proof as soon as the travel problem happens, especially anything that shows the official reason, timing, cost, and refund status.

Quick win: Before you leave the counter, clinic, baggage office, or provider chat, ask: “Can you put that in writing?”

What Not to Rely On by Itself

Some documents can support a claim, but may not be strong enough on their own.

A screenshot may show that a flight was delayed, but not the official cause. A receipt may show that you bought something, but not whether the expense was necessary or covered. A booking confirmation may show that a reservation existed, but not whether the amount was non-refundable. A personal explanation may describe what happened, but it may not replace proof from the airline, hotel, doctor, police department, baggage office, or travel provider.

Those documents can still help fill in the timeline. But if a key part of the claim depends on them, try to support them with stronger proof from the source of the problem.

Check the Fine Print

Not Sure What Could Weaken Your Claim?

Use the Travel Fine Print Risk Checker to narrow whether the issue is documentation, refund rules, policy exclusions, timing, booking terms, or another travel fine-print problem.

Travel Fine Print Takeaway

The strongest proof connects the whole claim story.

A strong travel insurance claim file does more than show receipts. It helps prove what happened, why it happened, what it cost, and what amount was not refunded, credited, reimbursed, or recoverable elsewhere.

❓Frequently Asked Questions

These questions explain what travel insurance claim proof usually needs to show before an insurer can evaluate the claim.

What proof do you need for a travel insurance claim?

The proof depends on the claim type, but it usually needs to show what happened, why it happened, what it cost, and what amount was not refunded, credited, reimbursed, or recoverable elsewhere. Common documents include claim forms, booking confirmations, proof of payment, receipts, medical records, airline notices, baggage reports, refund records, and provider statements.

Are receipts enough for a travel insurance claim?

Not always. Receipts can prove what you paid, but they may not prove why the expense happened, whether it was covered, whether it was necessary, or whether the cost was non-refundable. Stronger claims usually include receipts plus documents that explain the event and refund status.

Do you need proof of payment for travel insurance?

Often, yes. Insurers may ask for proof that you paid for the travel expense being claimed. This could include a receipt, invoice, booking confirmation, credit card statement, or other payment record. The document should connect the charge to the trip cost or expense being claimed.

What is proof of loss for a travel insurance claim?

Proof of loss is documentation that supports the reason and amount of the claim. It may include provider statements, medical records, cancellation confirmations, airline delay letters, baggage reports, refund denials, receipts, or other records showing what happened and what money was actually lost.

Can a travel insurance claim be denied for missing documents?

Yes. A claim may be delayed, reduced, or denied if the documents do not prove the covered reason, timing, eligible expense, or unrecovered loss. If the denial is based on missing or unclear proof, submitting better documentation may help with a resubmission or appeal.

Bottom Line

Travel insurance claim proof is not just about collecting paperwork.

It is about showing the full claim story clearly enough for the insurer to evaluate it.

A receipt may prove what you paid. A delay notice may prove something happened. A cancellation email may prove a trip component changed. But the strongest claim files connect the key pieces: what happened, why it happened, what it cost, and what amount was not recovered from another source.

That is why the best time to save proof is before you file — and often while the travel problem is still happening.

Before you leave the airline counter, baggage office, hotel desk, clinic, or provider chat, ask for written confirmation. Save receipts, records, refund details, and policy-related documents as you go.

The clearer the proof, the easier it is to show whether the claim fits the policy.

Related Guides

Keep this one tight because this article is a practical support page.

Travel Insurance and Claim Problems

- Why Travel Insurance Claims Get Denied — And What to Check Next

Why a claim may fail even when the travel problem was real. - Travel Insurance Claim Denied for Lack of Documentation? What to Check Next

Why receipts alone may not fix a documentation denial. - Does Travel Insurance Require Receipts? What They Do and Don’t Prove

Why receipts prove payment, but not always the covered reason or claim amount. - Does Travel Insurance Cover Passport Problems?

When passport issues may or may not be covered. - Does Travel Insurance Cover Forgetting Your Passport?

Why traveler mistakes are different from lost or stolen documents.

Refunds and Booking Rules

- Do You Need Travel Insurance If Your Flight or Hotel Is Refundable?

Why refundable bookings may not protect the whole trip. - Why Travel Refunds Take So Long

Why approved refunds may still take time.