You had a real travel problem.

Maybe your flight was delayed. Maybe your bags were lost. Maybe you had to cancel because of a medical issue. Maybe you paid for extra hotel nights, replacement clothing, medical care, transportation, or prepaid trip costs you could not recover.

Now the insurance company is asking for proof of loss.

That phrase can sound like another way of saying “send documents,” but it is more specific than that. The insurer is not only asking whether something went wrong. It is trying to verify whether the travel problem created a covered, measurable financial loss under the policy.

The real question is not just:

“What documents do I need for my travel insurance claim?”

It is:

“Do my documents prove what happened, why it happened, what it cost, and what amount was still unrecovered?”

This guide explains what proof of loss means in a travel insurance claim, why it is more than a document checklist, and how to organize proof around the covered event, financial loss, and amount that was not recovered elsewhere.

Quick Answer

Proof of loss is not just documentation. It is the claim math.

Proof of loss is the documentation that helps show what happened, why it happened, what it cost, and what amount was not recovered elsewhere. It may include receipts, invoices, medical records, airline delay letters, baggage reports, cancellation proof, refund denials, voucher records, credit notices, or other documents tied to the claim.

The important point is that proof of loss is not just a document checklist. A strong claim file connects the travel problem to a covered reason, a measurable cost, and an unrecovered amount that may be payable under the policy.

A proof-of-loss request can feel broad because different claim types need different documents. A flight delay claim will not look the same as a medical claim. A baggage claim will not look the same as a trip cancellation claim.

But the underlying question is often the same.

The insurer is trying to connect the travel problem to the financial loss. That means your documents should not only show that something happened. They should help show whether the event fits the policy, whether the expense was caused by that event, and whether the amount you are claiming was still your responsibility after refunds, credits, vouchers, or compensation.

System Insight

Proof of loss is about connecting the event to the amount being claimed.

- The event matters because the insurer needs to understand what actually happened during the trip.

- The cause matters because not every travel problem is a covered reason under the policy.

- The cost matters because the claim has to show a measurable financial loss.

- The unrecovered amount matters because refunds, vouchers, credits, compensation, or other benefits may reduce what the policy can pay.

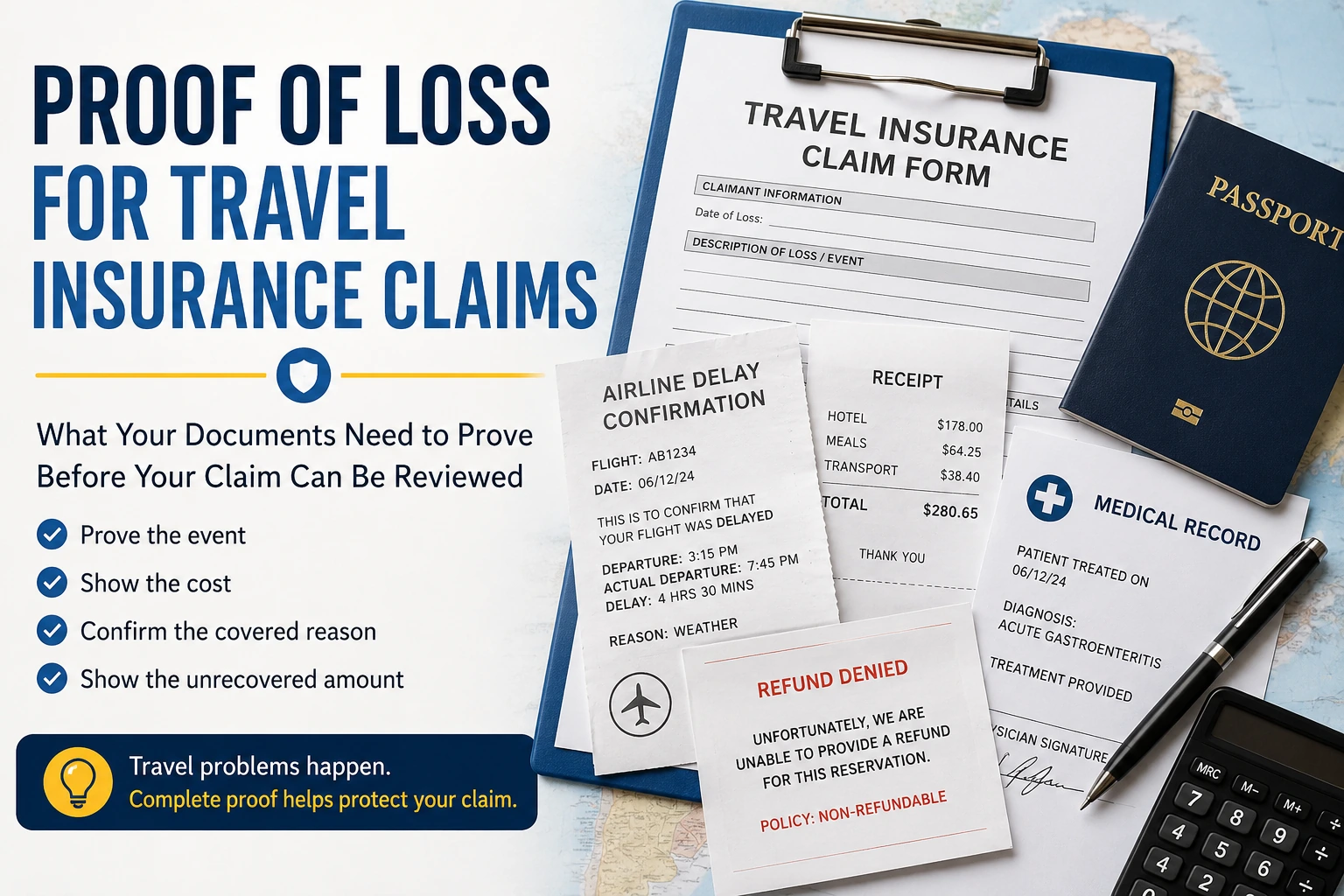

What Proof of Loss Needs to Show

Travel insurance proof of loss is not one single document. It is usually a group of documents that work together.

One document may prove the travel problem. Another may prove the cost. Another may prove that the airline, hotel, cruise line, tour provider, or credit card company did not already reimburse the loss.

Before you file, organize proof of loss around four questions:

Claim Proof Framework

The Four Parts of Proof of Loss

A stronger travel insurance claim does not just show that something went wrong. It connects the travel problem to a covered, measurable, unrecovered loss.

What happened?

Show the delay, cancellation, illness, injury, baggage issue, theft, interruption, or other event behind the claim.

Why did it happen?

Show the reason for the event, because the policy may cover some causes and exclude others.

What did it cost?

Show the financial loss with receipts, bills, invoices, prepaid trip costs, or replacement expense records.

What was not recovered?

Show what remained after refunds, vouchers, credits, compensation, provider adjustments, or other reimbursements.

That four-part structure matters because travel insurance claims are often reviewed as a chain.

If one part is missing, the claim may not be ready to evaluate. A receipt may show the cost, but not the cause. An airline delay notice may show the disruption, but not the extra expense. A cancellation email may show that the trip changed, but not whether the prepaid amount was non-refundable.

Proof of loss is strongest when the documents work together instead of sitting in separate, disconnected uploads.

Why Proof of Loss Is More Than Proof That Something Went Wrong

A common mistake is treating proof of loss as proof of the travel problem.

That is only part of it.

For example, an airline delay notice may show that your flight arrived late. But it may not show that the delay met your policy’s minimum time requirement, that the reason was covered, or that your extra meals, hotel, transportation, or missed prepaid costs are eligible.

A medical note may show that you were treated during the trip. But it may not show what the treatment cost, whether the expense was paid, whether another insurance plan should respond first, or whether the condition fits the travel policy’s rules.

A baggage report may show that your luggage was delayed or lost. But it may not show the value of the items, what emergency purchases were necessary, or whether the airline already paid compensation.

That is why claim files can feel frustrating. You may have documents, but the insurer may still ask for more because the file does not yet prove the full loss.

The Missing Piece Is Often the Unrecovered Amount

The part travelers often miss is the amount that was not recovered elsewhere.

Travel insurance generally does not pay a loss twice. If an airline refunded part of a ticket, issued meal vouchers, covered a hotel, or paid baggage compensation, that may reduce the amount left for the insurer to consider. The same can happen with hotel refunds, cruise credits, tour credits, credit card travel benefits, medical insurance payments, or provider adjustments.

That does not mean the claim is automatically denied. It means the claim file may need to show what was paid back, what was credited, what was denied, and what amount remained your responsibility.

This is where proof of loss becomes more than a receipt file. It becomes a loss calculation.

Traveler Risk

Your claim can stall if the documents prove the problem but not the loss.

A flight delay, medical issue, cancellation, or baggage problem may be real, but the insurer may still need proof of the covered reason, eligible cost, benefit limits, refunds, vouchers, credits, compensation, and remaining unrecovered amount before deciding what, if anything, is payable.

Check the Fine Print

Not Sure What Your Claim Documents Still Need to Prove?

Use the Travel Fine Print Risk Checker to review the type of travel problem, the documents you have, and whether your claim may still need proof of timing, cost, covered reason, or unrecovered loss.

Before You Submit Proof of Loss

The Risk Checker can help you spot possible proof gaps, but the best time to organize a claim is before you upload documents to the claim portal.

Do not think of proof of loss as a folder full of random receipts, emails, reports, and screenshots. Think of it as a claim story.

Each document should answer a question the insurer may need to evaluate: what happened, why it happened, what it cost, whether the policy benefit applies, and what amount was still unrecovered.

That does not mean every claim needs every document. It means every document should have a purpose.

Action Step

Build proof of loss around the claim questions.

Before you submit a travel insurance claim, organize your documents so they clearly connect the travel problem to the covered reason, cost, and unrecovered amount.

Quick win: For every document, ask: “Does this prove the event, the cause, the cost, or the unrecovered amount?” If it does not answer one of those questions, it may not close the proof gap.

Claim Proof Checklist

Check the proof before you file.

Use the travel insurance claim proof guide to review what your documents may need to show before you submit receipts, reports, letters, and refund records.

What Happens When Proof of Loss Has a Gap?

Incomplete proof of loss does not always mean the claim is denied immediately. Often, the insurer asks for more documents.

That can sound routine, but it can also slow the claim down. If the missing document is easy to get, such as a duplicate receipt or airline delay confirmation, the delay may be minor. If the missing document is harder to obtain, such as a medical statement, refund denial, police report, provider invoice, or proof that a prepaid cost was non-refundable, the claim can sit unresolved while you try to fill the gap.

The risk is that travelers sometimes submit a claim as soon as they have a few documents, then discover that the file does not yet prove the loss clearly enough.

Before you file, look for the weak link. If your documents show the event but not the cost, the claim may stall. If they show the cost but not the covered reason, the claim may stall. If they show both but not the unrecovered amount, the insurer may still ask what was refunded, credited, or paid by someone else.

A complete proof-of-loss file does not need to be complicated. It just needs to make the claim understandable.

Travel Fine Print Takeaway

Proof of loss is the bridge between the travel problem and the claim amount.

A travel problem may be real, and your documents may still be incomplete. Proof of loss should connect what happened, why it happened, what it cost, and what amount remained unrecovered after refunds, credits, vouchers, compensation, or other reimbursements.

The safest move is to build the claim file around the loss itself, not just around the documents you already have.

❓Frequently Asked Questions

These questions explain what proof of loss means for travel insurance, why it is different from a basic document checklist, and what may happen if your claim file is missing key proof.

What is proof of loss for travel insurance?

Proof of loss is the documentation that helps show what happened, why it happened, what it cost, and what amount was not recovered elsewhere. It may include receipts, invoices, medical records, airline delay letters, baggage reports, cancellation proof, refund denials, voucher records, or other claim documents.

Is proof of loss the same as a receipt?

No. A receipt may be part of proof of loss because it can show what you paid. But proof of loss usually needs more than proof of payment. The claim may also need documents showing the covered event, the reason for the loss, the timing, and whether any refund, credit, voucher, or compensation reduced the amount.

What documents can count as proof of loss?

It depends on the claim type. Proof of loss may include receipts, bills, invoices, trip confirmations, cancellation notices, airline delay letters, boarding passes, baggage reports, police reports, medical records, provider statements, refund denial emails, voucher records, and credit card statements.

Can a travel insurance claim be denied for missing proof of loss?

Yes. A claim can be delayed, reduced, or denied if the insurer cannot verify the covered reason, eligible cost, timing, benefit limit, or unrecovered amount. The travel problem may be real, but the claim still needs enough documentation to evaluate what is payable under the policy.

What should I do if the insurer asks for more proof of loss?

Read the request carefully and identify what part of the claim is missing. The insurer may be asking for proof of the event, proof of the cause, proof of payment, proof that a cost was non-refundable, or proof that another company did not already reimburse the loss.

Bottom Line

Proof of loss is not just a travel insurance paperwork requirement.

It is the part of the claim file that helps the insurer connect the travel problem to a covered financial loss. A receipt may show payment. A delay letter may show a flight disruption. A medical note may show treatment. A baggage report may show that luggage was delayed or lost.

But the claim usually needs the documents to work together.

The strongest proof-of-loss file shows what happened, why it happened, what it cost, and what amount remained unrecovered after refunds, credits, vouchers, compensation, or other reimbursements.

The fine print is simple:

Do not just prove that something went wrong. Prove the loss the policy is being asked to pay.

Related Guides

Travel Insurance Claim Proof

- Travel Insurance Claim Proof: What Your Documents Need to Prove

What claim documents need to show. - Travel Insurance Claim Denied for Lack of Documentation? What to Check Next

What to check if the insurer says your proof was missing or insufficient. - Does Travel Insurance Require Receipts? What They Do and Don’t Prove

Why receipts prove payment, not the whole claim. - Do You Need an Airline Delay Letter for Travel Insurance?

When a delay letter helps — and what it does not prove.

Travel Insurance and Claim Problems

- Why Travel Insurance Claims Get Denied — And What to Check Next

Why real travel problems can still fail as claims. - Does Travel Insurance Cover Passport Problems?

When passport issues may or may not qualify.

Refunds and Booking Rules

- Do You Need Travel Insurance If Your Flight or Hotel Is Refundable?

Why refundable does not always mean fully protected.